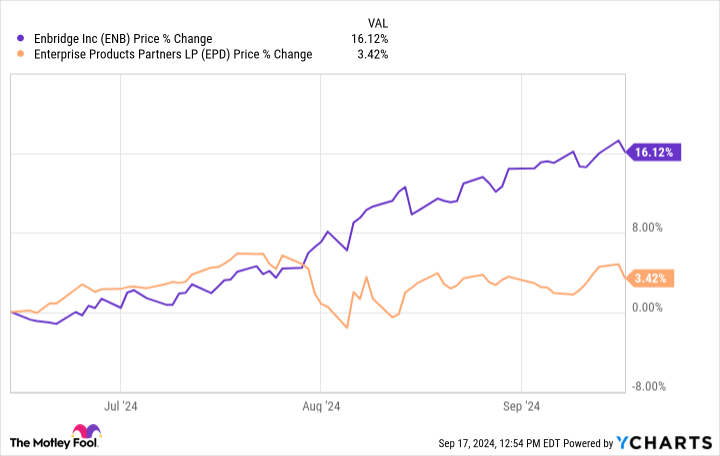

Share prices of Enbridge (NYSE: ENB) have risen 16% over the past three months as investors reassess the North American midstream giant’s future. But that rebound still isn’t enough to close the gap with fellow high-yield midstream giant Enterprise Products Partners (NYSE: EPD), which has recovered all its losses from a peak in mid-2022.

There’s likely to be additional recovery potential with Enbridge.

Recover: Enbridge versus Enterprise

Enterprise Products Partners is up just about 3.4% over the past three months, lagging well behind the 16% gain Enbridge’s stock has seen. If you just looked at this short-term performance, you’d probably suggest that Enterprise has more appeal.

But when you pull the lens back a bit further to encompass three years, the story changes dramatically.

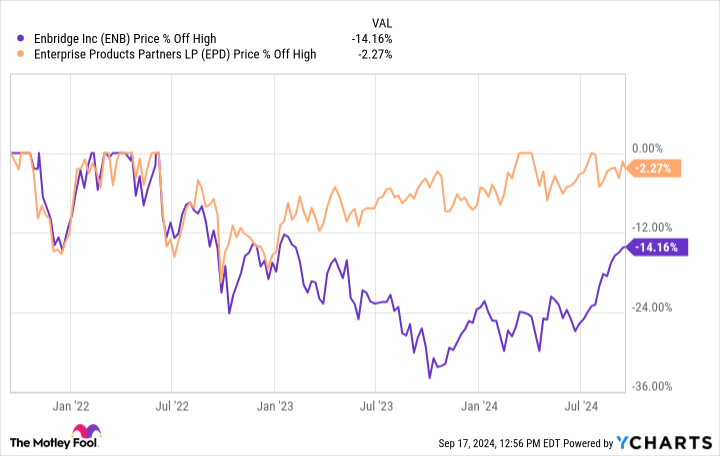

Over the past three years, you see that Enterprise and Enbridge both hit peaks in mid-2022. They both fell after the peak, but Enbridge’s decline was much more dramatic. It also lasted longer. Thus, the Canadian midstream giant’s recovery didn’t start until later, and the shares had more losses to recover. So, in this way, it makes sense that the last three months have been better for Enbridge’s shares than for Enterprise’s units.

But there’s one more important piece from the above graph. Enterprise in 2024 has recovered all of what it lost and trades near prior highs, while Enbridge still has more room to run before it gets to that point. The difference between the recovery of these two midstream players is about 12 percentage points.

If you are looking for a mix of yield and growth, that probably gives Enbridge the edge right now. That said, on the income front, Enbridge’s dividend yield is roughly 6.6% versus a 7% distribution yield for Enterprise. So, if all you want is income, you might favor Enterprise.

What’s the backstory with Enbridge?

The story here is fairly interesting. Enterprise is basically laser-focused on the midstream sector. Enbridge’s long-term goal is to shift its portfolio along with the world’s energy needs. While most of its business is tied to midstream assets, like pipelines, it also owns natural gas utilities and renewable energy facilities, like offshore wind developments. The company’s regulated utility operations are a key focus today as it completes and integrates the acquisition of three large regulated U.S. natural gas utilities from Dominion Energy (NYSE: D).

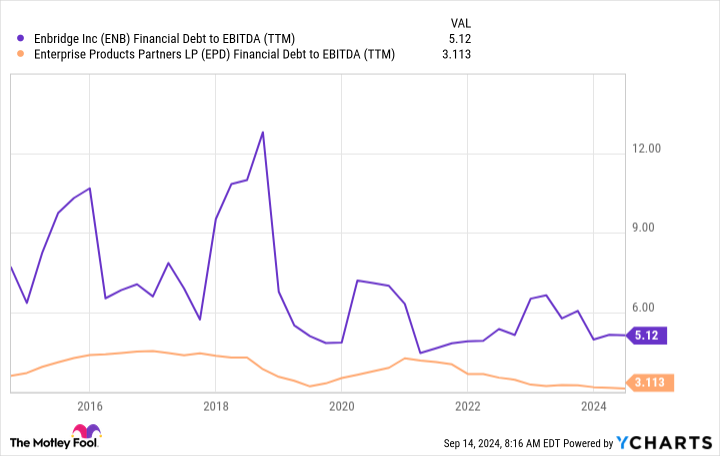

There are two important takeaways. Because of its utility operations, Enbridge tends to make heavier use of leverage than other midstream players, like Enterprise. In fact, Enterprise has long operated with a very modest level of leverage on its balance sheet. When interest rates were on the rise, investors were simply more worried about Enbridge than Enterprise, and thus, the stock of Enbridge performed worse.

But Enbridge also agreed to buy those natural gas utilities from Dominion. There were concerns about how it would fund the purchase price, leading to more downward pressure on the shares. This is a key reason Enbridge’s stock fell so far and hard.

Now, however, Enbridge has proven it was able to manage the cost of acquiring the utilities (without blowing up its balance sheet), and interest rates look likely to start falling. So, there’s a double tailwind behind Enbridge’s stock, with more room to run before it gets back to where it was before the current sell-off.

Enbridge has a solid future ahead

With nearly three decades of annual dividend increases under its belt, Enbridge has proven it is a reliable dividend stock. Although the yield is lower right now than that of Enterprise, don’t let that cloud your view of Enbridge. It is still an attractive dividend stock, and unlike Enterprise, there’s still material recovery potential for the shares.

If you buy it, though, don’t just think about that short-term opportunity. It’s a high-yield dividend stock you can comfortably keep in your portfolio forever. Remember, unlike Enterprise, Enbridge is actively adjusting its portfolio to serve the world’s energy needs as they change.

Should you invest $1,000 in Enbridge right now?

Before you buy stock in Enbridge, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Enbridge wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $715,640!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 16, 2024

Reuben Gregg Brewer has positions in Dominion Energy and Enbridge. The Motley Fool has positions in and recommends Enbridge. The Motley Fool recommends Dominion Energy and Enterprise Products Partners. The Motley Fool has a disclosure policy.

1 Magnificent High-Yield Stock Down 14% to Buy and Hold Forever was originally published by The Motley Fool