C3.ai (NYSE: AI) was one of the world’s first enterprise AI companies. It was founded in 2009, and it currently has a portfolio of over 40 ready-made software applications designed to help businesses accelerate the adoption of artificial intelligence (AI).

C3.ai made a significant change to its business model two years ago, and it’s starting to pay off in the form of accelerating revenue growth. However, its stock remains 87% below its all-time high, set during the 2020 tech frenzy.

C3.ai stock was unquestionably overvalued then. But the company’s strong growth, combined with the substantial financial opportunity in the AI industry, make it look like a very good value right now. Here’s why investors with a spare $25 might want to allocate it to buying one share of C3.ai.

A unique way to play the AI boom

C3.ai serves businesses across 19 industries, many of which wouldn’t typically be associated with cutting-edge technologies like AI. They include manufacturing, oil and gas, utilities, and more. It’s because C3.ai offers a unique value proposition — the company can deliver tailored AI solutions to customers in as little as three months following an executive briefing.

Oil and gas giant Shell, for example, deployed over 100 C3.ai applications across its organization. They’re used to monitor over 10,000 items of equipment for predictive maintenance, which reduces the probability of a catastrophic failure. Plus, at one of Shell’s liquefied natural gas plants, C3.ai’s asset optimization software reduced carbon emissions by 355 tons per day. That’s the equivalent of taking 28,000 vehicles off American roads.

C3.ai sells its AI software directly to customers, but it also has sales partnerships with tech giants like Microsoft, Amazon, and Alphabet. They offer C3.ai’s applications on their cloud platforms, placing them in front of millions of customers the company might not have had access to otherwise.

During the fiscal 2025 first quarter (ended July 31), C3.ai closed 51 agreements through its partner network, a 155% increase from the year-ago period. They accounted for 72% of C3.ai’s total deal flow, which highlights the importance of its partnerships.

Accelerating revenue growth

C3.ai generated a record $87.2 million in revenue during Q1, representing a 21% increase from the year-ago period. It also marked the sixth consecutive quarter of accelerating growth, which is a direct result of a strategy shift inside the company two years ago.

At the beginning of C3.ai’s fiscal 2023 year (which started May 1, 2022), the company told investors it would switch from a subscription-based revenue model to a consumption model. The goal was to eliminate lengthy negotiating periods with customers, allowing them to join C3.ai with less friction and allowing them to pay only for what they use.

The company warned investors the strategy shift would lead to a temporary slowdown in its revenue growth while it transitioned its existing customers to the new model. Near the end of fiscal 2023, its revenue actually started to shrink compared to the year-ago period. However, the assumption was that consumption pricing would lead to much faster customer acquisitions, which would drive an acceleration in revenue growth in the future. That’s what appears to be happening now.

C3.ai’s accelerating growth is more impressive when you consider the company is carefully managing its costs to improve its bottom line. That means it’s spending less aggressively on growth-oriented initiatives like marketing. C3.ai’s total operating expenses only grew by 8.8% year over year during Q1. Since revenue grew more quickly, that led to a 2.4% reduction in its net loss from the year-ago period, to $62.8 million.

On a non-GAAP basis, however, C3.ai’s net loss was only $6.8 million. The company issued $54.6 million in stock-based compensation to its employees during the quarter (which is a non-cash expense). Stripping C3.ai’s bottom line down even further shows that it delivered $7.1 million in free cash flow.

The company has $762 million in cash, equivalents, and marketable securities on its balance sheet, so generating positive free cash flow will protect that position and reduce the likelihood it will need to raise capital in the near future.

Why C3.ai stock is a buy now

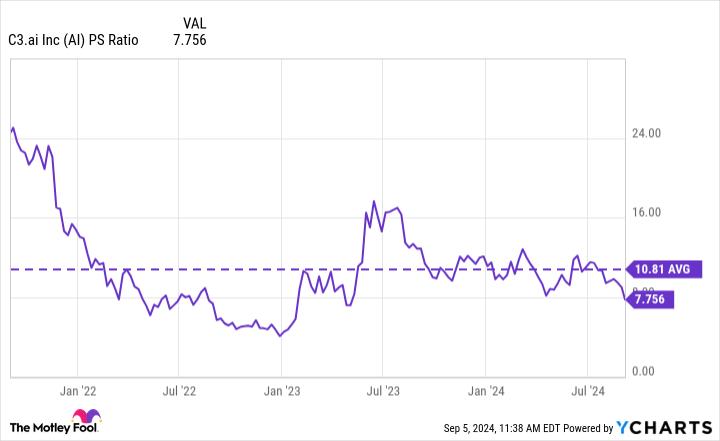

C3.ai came public in December 2020, during a frenzy in the technology sector driven by trillions of dollars in pandemic-related U.S. government stimulus spending, and record low interest rates. C3.ai’s share price peaked at $161 that very month, at which point it traded at an eye-popping price-to-sales (P/S) ratio of around 80.

The 87% decline in its stock price, plus the company’s revenue growth since then, pushed that P/S ratio down to just 7.7. That’s currently 29% below its three-year average of 10.8 (which excludes the lofty heights from the 2020 period).

Since C3.ai’s revenue growth is currently accelerating, I would argue it should be trading above its average P/S ratio — especially since management’s guidance for the upcoming fiscal 2025 second quarter (ended Oct. 31) points to a further acceleration in revenue growth, to as high as 28%.

According to a recent survey by PwC, around 70% of top corporate executives expect AI to significantly change the way their organization creates value over the next three years. Not all of those companies will be able to develop AI from scratch, so many will seek solutions like those offered by C3.ai. PwC also expects AI to add $15.7 trillion in value to the global economy by 2030, so the financial opportunity is enormous.

Investors might want to take advantage of the steep decline in C3.ai stock by adding it to their portfolios, because the coming decade could be transformational for the company.

Should you invest $1,000 in C3.ai right now?

Before you buy stock in C3.ai, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and C3.ai wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $630,099!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 3, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, and Microsoft. The Motley Fool recommends C3.ai and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

1 No-Brainer Artificial Intelligence (AI) Stock to Buy With $25 and Hold for 10 Years was originally published by The Motley Fool