Each quarter, hedge funds that manage over $100 million are required to file a Form 13F with the Securities and Exchange Commission (SEC). These filings break down which stocks investment firms bought and sold during the most recent quarter.

Ken Griffin is a billionaire investor who serves as CEO of the hedge fund Citadel. Last quarter, Citadel bought 7.9 million shares of Pfizer (NYSE: PFE) — increasing its stake in the pharmaceutical giant by 63%.

The last few years have featured a lot of ups and downs for Pfizer. While shares have posted break-even returns so far in 2024, Pfizer stock has cratered by more than 30% over the last three years.

Below, I’ll outline some of the bigger factors that have been weighing on Pfizer while also sharing my thoughts on what may have influenced Citadel to load up on the stock.

What is causing Pfizer stock to drop?

I see three major influences that have contributed to Pfizer’s beaten-down stock price.

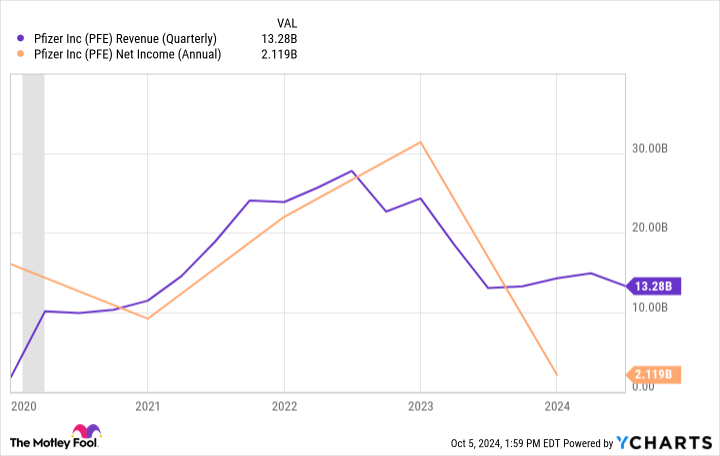

1. COVID-19: Along with Moderna and Johnson & Johnson, Pfizer played an instrumental role in developing vaccines that combated the COVID-19 virus. In the chart below, the grey shaded column represents the short-lived COVID-19 recession.

Between 2020 and 2022, Pfizer’s revenue and profits soared thanks in large part to the company’s COVID-related medications, Comirnaty and Paxlovid. However, since the fourth quarter of 2022, Pfizer’s growth has witnessed a noticeable deceleration due to falling demand for these COVID treatments as the world emerged from peak pandemic conditions.

2. Acquisitions: In an effort to combat stalling growth and diversify its product offerings, Pfizer acquired oncology specialist Seagen for $43 billion back in December 2023. While revenue from Seagen will help offset the declining sales of Comirnaty and Paxlovid, acquisitions often take years of integration efforts before they are fully accretive.

3. Road map: One risk to always keep in mind with pharmaceutical stocks is that these companies face patent cliffs on their medications. Over the next few years, Pfizer expects to face patent challenges over some of its biggest drugs, including Eliquis, Ibrance, Prevnar 13, and Xtandi. Although it’s difficult to know how much Pfizer’s growth will be impacted as generic alternatives to these treatments hit the market, the company could very well lose out on billions in sales.

Something else may be lingering in the background

Considering sales from Pfizer’s blockbuster COVID treatments are declining combined with billions more in revenue at stake thanks to expiring patents, what else can Pfizer do to offset these risks besides inorganic growth derived from acquisitions?

One hot area in the healthcare realm that Pfizer has been eyeing for some time is weight loss. Glucagon-like peptide-1 (GLP-1) agonists such as Ozempic, Wegovy, Rybelsus, Saxenda, Mounjaro, and Zepbound have been transformative growth drivers for their developers, Novo Nordisk and Eli Lilly.

The global total addressable market (TAM) for GLP-1s is expected to reach $100 billion by 2030, according to research from Goldman Sachs. Although Lilly and Novo Nordisk dominate the GLP-1 space at the moment, a number of other pharmaceutical companies of varying sizes are competing to break into the market.

While it’s still early days for Pfizer’s GLP-1 candidate, Danuglipron, recent clinical testing has indicated the drug is well tolerated.

The bottom line

Considering the unknowns surrounding Pfizer’s business as it relates to offset declining sales from COVID medications, the vulnerability presented by patent cliffs, and the multi-year timeline surrounding large-scale acquisitions, I’m not surprised to see Pfizer stock continue sliding.

Right now, Pfizer trades at a forward price-to-earnings (P/E) multiple of just 10.8. To put this into perspective, this is less than half of the S&P 500 index’s forward P/E multiple of 23.2.

I think the current trading activity surrounding Pfizer stock paints a clear picture; many investors are thinking about the short-term risks instead of longer-term prospects. Another way of looking at it is that the potential gains from Danuglipron combined with growth from Seagen could more than offset any losses from other medications in the long term.

Pfizer’s contracting valuation and its potential to enter the new markets may be what is compelling Citadel to continue buying the stock.

With all of this said, it is going to take years before Pfizer hits its stride in the oncology treatment market. Moreover, there is no guarantee that its ambitions in the weight loss realm will ever come to fruition, as much more testing with the Food and Drug Administration (FDA) will be required before Danuglipron potentially hits the market.

Should you invest $1,000 in Pfizer right now?

Before you buy stock in Pfizer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Pfizer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $814,364!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 7, 2024

Adam Spatacco has positions in Eli Lilly and Novo Nordisk. The Motley Fool has positions in and recommends Goldman Sachs Group and Pfizer. The Motley Fool recommends Johnson & Johnson, Moderna, and Novo Nordisk. The Motley Fool has a disclosure policy.

Billionaire Ken Griffin Just Bought 7.9 Million Shares of This Beaten-Down Pharmaceutical Stock as It Eyes the Weight Loss Market was originally published by The Motley Fool