Companies that decide to split their stock — increasing share count and decreasing per-share price — are usually doing quite well. Most companies don’t announce stock splits unless their shares have climbed significantly over time.

However, there are occasions when a stock split occurs during a rocky period for the company’s shares. This is the case for Super Micro Computer (NASDAQ: SMCI), whose stock is down 35% since its split announcement in early August.

Still, many analysts on Wall Street believe there is massive potential for Supermicro. So, is it time to buy?

Supermicro’s business is booming

On Sept. 25, a group of 16 analysts had an average one-year price target on Supermicro stock of $729.19. That represents around 60% upside from the stock’s closing price on Sept. 25, which was a day before a Wall Street Journal article helped fuel a 12% drop.

The optimism makes sense. Super Micro Computer manufactures components for computing servers. While this space is relatively crowded, Supermicro sets itself apart from the competition by offering highly customizable servers that can be tailored to any workload type or size. Its products are also some of the most energy-efficient ones out there, which can save on long-term operating costs.

With the massive spike in computing demand caused by the artificial intelligence (AI) arms race, Supermicro is benefiting from the same trends that sent Nvidia stock through the roof, though Supermicro’s ride has been a bit more bumpy.

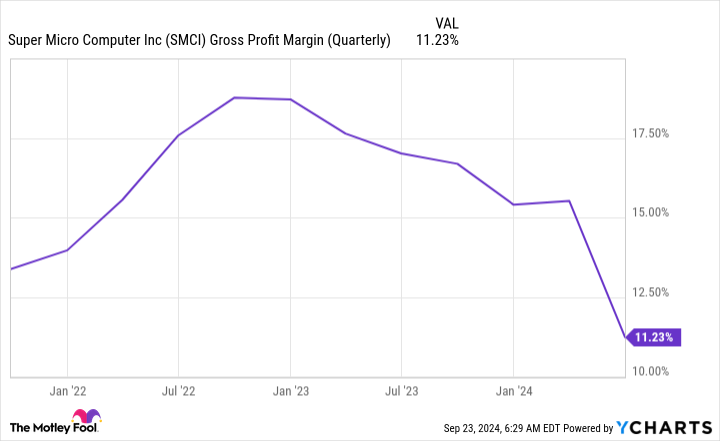

Supermicro is not firing on all cylinders right now

Along with Supermicro’s 10-for-1 stock-split announcement on Aug. 6, the company released its fiscal 2024 fourth-quarter and full-year results for the period ended June 30. While the company delivered strong revenue growth of 143% year over year and provided excellent full-year 2025 guidance of 74% to 101% growth, there were some problems with its profitability.

Because of its new liquid-cooling product line getting spun up, Supermicro’s gross margin has taken a hit.

This has caused significant concern among some investors as falling gross margin can also indicate increased competition. However, management believes its gross margin will recover throughout fiscal 2025.

Meanwhile, short-selling firm Hindenburg Research released a report on Supermicro on Aug. 27 alleging accounting manipulation. The SEC has fined Supermicro for accounting issues in the past. At the same time, because Hindenburg is a short-seller, it benefits when the stocks it reports on fall, so investors should proceed cautiously with this information. Supermicro responded that the short report “contains false or inaccurate statements.”

On Aug. 28, Supermicro delayed filing its end-of-year Form 10-K with the SEC, saying it needed more time to “complete its assessment of the design and operating effectiveness of its internal controls over financial reporting.”

After the delay, Supermicro received a letter of non-compliance from the Nasdaq exchange, stating it is in violation of listing rules because it hasn’t filed its 10-K in a timely fashion. After receiving the letter on Sept. 16, Supermicro has 60 days to comply or risk being delisted.

To further complicate matters, on Sept. 26, The Wall Street Journal reported that unnamed sources had said the Department of Justice had launched a probe into the company. If the reporting is correct, this is just a preliminary probe, so nothing may come out of it. However, there could be real issues with the company, which significantly increases the risk of investing in the stock. It will likely be a long time before the public gets full details, so investors will need to stay patient with the stock if they choose to buy it.

Clearly, the company is grappling with serious issues right now, and the stock has fallen over 60% from its 52-week high. However, the business case for its components and servers is undeniable.

The current stock is also valued fairly cheaply on a forward earnings basis.

If Supermicro can improve its gross margin over the next year and dispel concerns over its accounting practices, the stock has a ton of upside.

I recently bought the dip because I believe in the company. However, I kept the position size low (around 1% of my total portfolio value). That way, it won’t affect the portfolio too much if the stock tumbles further, but I can still benefit if Supermicro stages a recovery like some on Wall Street think it can in the near term. I was planning on buying more, but after the report of a potential DOJ probe, I’m comfortable with the current position size, as it represents the high risk, high reward associated with Super Micro Computer’s stock.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $760,130!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 23, 2024

Keithen Drury has positions in Super Micro Computer. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

Is Stock-Split Stock Super Micro Computer Headed to $729 per Share? was originally published by The Motley Fool