Li Auto (LI) stock hasn’t rewarded investors much in 2024, with the unsuccessful launch of its first all-electric vehicle and a downturn in Q1 deliveries. However, things have picked up significantly since March, and more central government stimulus might aid this domestic market-focused manufacturer. I’m still bullish, noting a strong delivery outlook and impressive margins.

How China Stimulus Impacts Li Auto

For those of you who are new to Li Auto, it’s a Beijing-based New Energy Vehicle (NEV) company. The firm is focused on the production of Extended Range Electric Vehicles (EREVs). These are essentially hybrids, mixing battery technology with traditional combustion engines. This results in extremely impressive claimed ranges for the vehicles, supporting my optimistic view. For example, Li says its L6 can support a CLTC range of 1,390 kilometers.

The stock has suffered in 2024 following the disappointing launch of its first 100% battery electric vehicle (BEV), the Li Mega, which saw lower than expected deliveries in Q1. However, deliveries have picked up in Q2 and Q3. Through early September, so far this year Li Auto has delivered 288,103 vehicles, up nearly 40% from 2023.

Li Auto stock, along with most of the Chinese market and Chinese stocks listed overseas, surged on Tuesday, September 24 after Beijing announced a series of stimulus measures. The economic stimulus, including interest rate cuts and reduced reserve requirements for banks, may help Li via mechanisms related to increased consumer spending power and confidence. Likewise, measures targeting the property market may also indirectly benefit Li Auto by improving overall economic sentiment.

Li Auto’s Delivery Growth Remains Impressive

Despite LI stock recently surging after the government’s stimulus announcement, it’s still down 34.4% year to date. And while I understand the disappointment that Q1 brought, with the (rather ugly) Li Mega flop, and sales far below Q4 2023, I believe the stock has been oversold by investors. I present two reasons for this belief.

First, I’m encouraged by the strong recovery in deliveries. In July, Li delivered 51,000 cars, marking a monthly record. An impressive recovery in deliveries is being driven by its least expensive model — the L6. Deliveries of this model exceeded 20,000 units for a third consecutive month in August.

Li Auto management has predicted a continuation of this trajectory. The company has guided to deliveries of between 145,000 and 155,000 vehicles in Q3, representing growth of 38% to 47.5%. That’s around 50,000 vehicles per month. Meanwhile, peers, Nio (NIO) and Xpeng (XPEV) are expected to grow deliveries by 14% and 13% respectively in Q3. On September 19, the company announced the 100,000th delivery of the L6, demonstrating just how important the vehicle has been to recent momentum.

Li Auto Is Winning on Margins

Li Auto is leading the pack when it comes to vehicle margins among Chinese EV start-ups. In Q2, the company reported an impressive 18.7% margin, significantly outperforming competitors like NIO and XPeng as well as more established peers like Tesla (TSLA) and BYD (BYDDF). While there was a slight quarter-over-quarter decline, Li Auto still maintains a substantial lead in this important metric.

For context, NIO’s Q2 vehicle margin was 12.2%, while XPeng trailed the group with margin of 6.4%. This means Li Auto’s margins were 53% higher than NIO’s and almost 3x those of XPeng. These strong margins, combined with Li Auto’s profitability and robust delivery outlook, make it a standout in the competitive NEV market.

Despite the challenges faced by EV start-ups, including intense competition and potential margin pressures, Li Auto’s performance suggests it’s well-positioned for success. Higher margins also point to a lower-risk investment.

Li Auto Isn’t Expensive

Despite all of the aforementioned positives, Li Auto stock isn’t expensive. In fact, it trades at a discount to the vast majority of its peers. As compared to its profit-making peers, Li Auto’s forward price-to-earnings (P/E) ratio of 21.5x is a small premium to BYD’s multiple of 19.8x, and substantially lower than Tesla’s 108x P/E.

With regards to the companies that are yet to turn a profit, I strongly believe that Li is massively undervalued. Li’s forward EV-to-sales ratio is just 0.65x, versus 1.45x at Nio, 2.03x at Rivian (RIVN), and 1.63x at Xpeng. I’d also like to highlight Li’s very strong cash position. The company has a net cash position of $11.25 billion, that is much stronger than all of its peers including BYD.

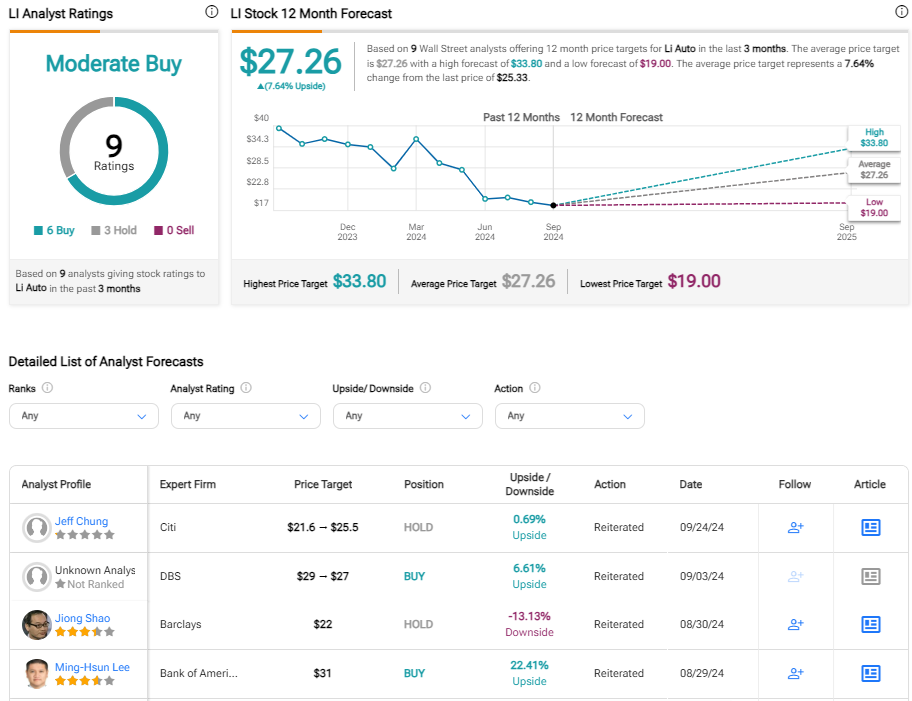

Is Li Auto Stock a Buy, According to Analysts?

On TipRanks, LI stock comes in as a Moderate Buy based on six Buys, three Holds, and zero Sell ratings assigned by analysts in the past three months. The average Li Auto stock price target is $27.26, implying a about 8% potential upside.

The Bottom Line on Li Auto Stock

I believe that Li Auto stock can continue its climb higher. I’m encouraged by the company’s industry-topping margins and its strong delivery outlook. The recent introduction of new stimulus measures by the Chinese government could further fuel Li Auto’s business by stimulating domestic demand.