Palantir Technologies (NYSE: PLTR) continues to rack up new contracts. The latest is a deal with the U.S. government to bring artificial intelligence (AI) capabilities to the various military branches through its Maven Smart System. The contract will pay Palantir up to $99.8 million over the next five years.

With the company announcing several new contract wins, many investors are wondering if these contract awards will be enough to fuel the growth needed to justify the company’s high valuation. Let’s see if an answer presents itself.

Valuation versus growth

Palantir established itself as a top data analytics and AI tech company that helps the government in some of its most important mission-critical tasks. Its services have been used to fight terrorism and track COVID-19 cases during the pandemic. More recently, it has seen a lot of growth in the private sector as customers adopt its Artificial Intelligence Platform (AIP) to address their various use cases.

Palantir’s success in the private sector extends across industries. Its recent contracts include work for the health system Nebraska Medicine and energy giant BP. The company is getting a lot of traction with commercial customers for its AI platform, with its commercial segment seeing 33% year-over-year revenue growth in the second quarter to $307 million.

Its overall government segment had shown signs of slowing in the past, growing only 14% in 2023. But it is picking up this year, with 16% growth in Q1 accelerating to 23% year-over-year growth in Q2 to reach $371 million for the quarter. Its U.S. government segment growth, meanwhile, went from just 12% year over year in Q1 to 24% in Q2. Overall, Palantir reports solid growth that is accelerating, with Q2’s overall revenue growth hitting 27% to $678 million.

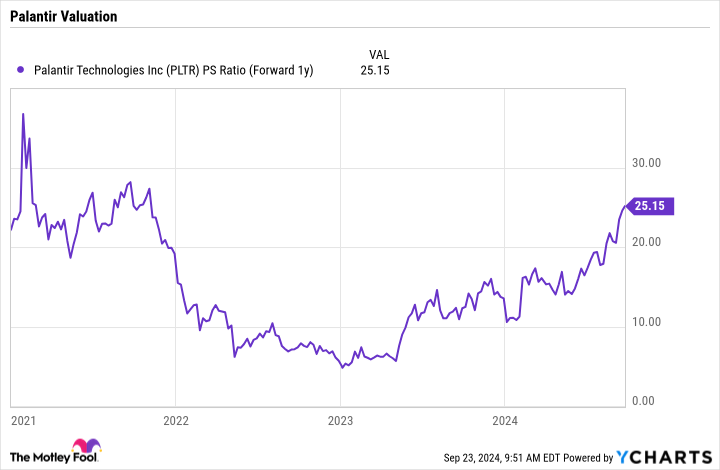

When it comes to the stock, the company’s revenue growth still doesn’t quite justify its current valuation. Its forward price-to-sales (P/S) ratio sits at 25 times analysts’ 2025 consensus revenue estimates.

That is the type of valuation that is typically reserved for hyper-growth stocks that expect 50% or more revenue growth over the next few years. Palantir needs to see its growth continue to accelerate if it wants to justify the stock’s current valuation.

A deal like the one it just signed with the military for its Maven Smart System will add about $20 million a year in revenue. The company has forecast revenue of between $2.742 billion and $2.750 billion this year, so $20 million isn’t moving the needle too much, adding about 0.7 percentage points of growth.

This is a large deal, but the company will need a lot more big U.S. government contracts to really help accelerate growth. One way it could do this is by teaming up with Microsoft, as it will now be able to deploy its offerings through Microsoft’s government cloud, including Microsoft Azure Government, Azure Government Secret, and Azure Top Secret cloud. The government isn’t known to make the quickest decisions, and Palantir is hoping this partnership will help it speed up deployments with the U.S. government, especially with AIP.

On the commercial side, the company will continue to look to grow its customer base through its use of boot camps, which show customers how AIP can be applied to potential use cases while providing onboarding and training. The company has been winning many customers for prototype work with this go-to-market strategy, which it then has been moving to production.

This transition from prototype to production is where Palantir sees its biggest opportunity, and the company has been doing a great job of growing business with existing commercial customers as a result.

Valuation still matters

The problem, though, still comes down to valuation. If Palantir were able to grow revenue by 30% in each of the next three years (a rate higher than its current revenue growth), it would result in $6 billion in revenue in 2027. That revenue total would result in a forward P/S multiple of about 14 using the current stock price.

With 30% revenue growth, that 14 P/S could be justified and would be similar to a company like CrowdStrike. However, it would also mean that Palantir’s stock traded flat over the next two years. It is also asking a lot to see the company generate 30%-a-year revenue growth over the next three years when it generated 24% revenue growth in 2022, 17% revenue growth in 2023, and 24% through the first six months of this year.

While Palantir has the makings of being a great company, valuation does still matter, and Palantir’s valuation is just too high to justify buying right now.

Should you invest $1,000 in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $740,704!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 23, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends BP, CrowdStrike, Microsoft, and Palantir Technologies. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Palantir Just Won Another Large Contract. Is It Enough to Make the Stock a Buy? was originally published by The Motley Fool