It’s tempting to gravitate toward dividend stocks that pay huge dividends. Take Walgreens Boots Alliance (NASDAQ: WBA) for example. The pharmacy chain’s dividend yields over 11% at its current share price. In other words, investors get double-digit investment returns before factoring in any potential share price movement.

However, there is never a free lunch in the stock market. It’s rarely so easy.

Peek behind the curtains and you’ll will find a litany of issues at Walgreens that have created such a high dividend yield. This is a warning sign of a yield trap.

Here are three problems facing Walgreens and why dividend-hungry investors may want to look elsewhere.

1. Junk-status financials may trigger a dividend cut

Many consumers may already be familiar with Walgreens Boots Alliance. The company has a sprawling network of pharmacies across America, Europe, and Latin America under the Walgreens and Boots brands. The traditional pharmacy model worked wonders for years; companies like Walgreens would fill prescriptions and use the foot traffic to sell groceries and other goods to help boost their profit margins.

Unfortunately, the digital age has begun impacting this business model, and Walgreens has sought to evolve with the times by using mergers and acquisitions to grow larger and diversify its business model. It merged with Boots Alliance in 2014 to expand its store footprint and then acquired VillageMD in 2021 to enter primary care services.

It hasn’t turned out well; the company has struggled under a massive debt load, and cash flow has dried up significantly. In July, S&P Global downgraded Walgreens’ credit to BB, a sub-investment-grade rating (junk status). The company is now scrambling to clean up its financials and it may sell its VillageMD business. Walgreens slashed the dividend nearly in half in early 2024, so don’t be shocked if it happens again: It still costs Walgreens over $200 million quarterly.

2. The S&P 500 could soon drop the company

How likely is it that another cut is on the way? The chances seem pretty high. Don’t underestimate the stigma attached to junk status financials. Walgreens is still a member of the S&P 500 index, a badge of honor that will probably be hard to get back once lost.

Investors generally favor S&P 500 companies, and having that status attracts institutional investors, especially funds that track the S&P 500, which must own the stock if it’s in the index. A stock can enjoy a boost from buyers when it’s added and could see additional selling pressure if removed.

Walgreens is already trading near multidecade lows, and the deteriorating financials only increase the chances that the index will remove Walgreens. The S&P 500 rebalances quarterly, and Walgreens lost its spot in the Dow Jones Industrial Average earlier this year.

3. Consumer health trends working against Walgreens

Walgreens must turn itself around to avoid all these negative consequences. However, doing so will require more than shedding debt. Walgreens must have a viable long-term business model. Unfortunately, the traditional pharmacy model is becoming dated; that’s why Walgreens set out on this acquisition spree in the first place.

Today, pharmaceutical drugs are starting to bypass retail pharmacies. Telehealth companies like Hims & Hers are enjoying rampant growth, and e-commerce giant Amazon has pushed into healthcare via its online service, including prescription delivery.

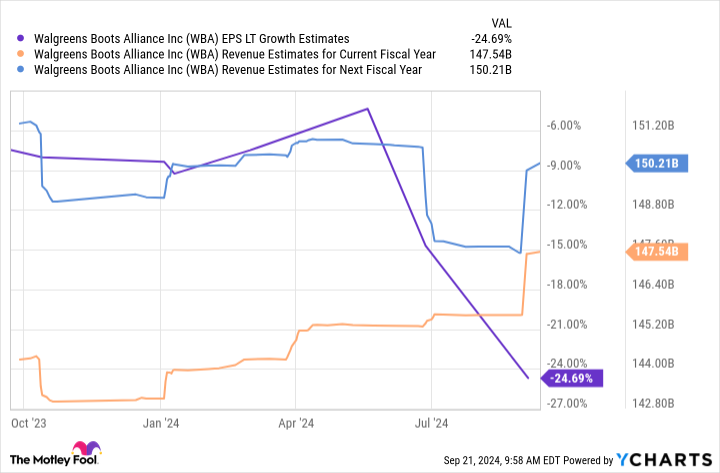

Analysts are currently pessimistic about Walgreens’ growth outlook. Estimates call for negative long-term earnings growth and low-single-digit revenue growth:

Walgreens more closely resembles a company barely holding on than a comeback story in motion. Dividends require healthy businesses to sustain them, and Walgreens isn’t there. Investors should avoid Walgreens stock and look for more durable dividend opportunities elsewhere.

Should you invest $1,000 in Walgreens Boots Alliance right now?

Before you buy stock in Walgreens Boots Alliance, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Walgreens Boots Alliance wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $712,454!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 23, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Justin Pope has positions in Hims & Hers Health. The Motley Fool has positions in and recommends Amazon and S&P Global. The Motley Fool has a disclosure policy.

Should You Buy Walgreens Boots Alliance for Its 11.1% Dividend Yield? 3 Things to Know First was originally published by The Motley Fool