Investors know what Warren Buffett’s favorite stocks are. He often talks about Coca-Cola and American Express, his two longest-held stocks, and he recently added Apple as a stock he’d never (fully) sell.

But Berkshire Hathaway has a full list of about 45 stocks, and some of them don’t get enough attention. Consider Ulta Beauty (NASDAQ: ULTA). This is a new Buffett stock, and he and his team were likely drawn to it right now because of its cheap price. But obviously, there’s a lot more to the investing thesis than that.

Let’s take a closer look.

A huge market opportunity

Ulta isn’t a surprising Buffett stock. It fits most of the typical Buffett criteria: excellent management, a dominant position in its industry, a competitive edge, and a cheap price.

It operates a national chain of beauty stores, but it’s differentiated in its model, and customers love it. Ulta bridges the gap between mass brands, traditionally sold in pharmacies and discount stores, and luxury brands, typically sold in upscale department stores. It caters to the beauty enthusiast by housing 600 brands under one roof and on its website.

It also offers beauty services, making it a complete, one-stop beauty shop. The full range of products and services increases overall engagement and loyalty, and Ulta has skyrocketed to the top of the industry.

Beauty is a fast-growing industry with sales increasing 10% year over year globally in 2023, according to McKinsey. Sales surpassed expectations and as well as other industries like apparel. In the U.S., Ulta’s domain, sales were up 9%. McKinsey expects sales to increase at a compound annual growth rate (CAGR) of 6% through 2028.

Beauty enthusiasts account for 83% of beauty product dollars spent, putting Ulta squarely in the middle of growing trends. Ulta believes there are 70 million such enthusiasts in the U.S., and it continues to attract them to its loyalty program, which reached 43 million last year. They represent 95% of Ulta sales, and this gives the company a huge data pool to meet demand as it grows and changes.

With nearly 1,400 stores and more to come, Ulta should benefit from industry growth. But it also continues to stretch its position with new products, brands, and collaborations, such as Target “stores within stores.”

Still waiting out the economy

The pitfall to offering the kitchen sink of beauty brands is that with inflation and tight pockets, customers are switching down to cheaper brands. However, since Ulta sells both, it’s still getting those dollars. It’s retaining its loyal customers and it’s well-positioned to rebound as inflation cools.

Total sales increased 4% year over year in the fiscal second quarter (ended Aug. 3), but comparable sales were down 1.2%. Gross margin fell from 39.3% to 38.3%, and operating margin fell from 15.5% to 12.9%. These were continuing trends, but they were worse than expected. Management revised guidance lower across the board.

It’s not surprising that Ulta stock is down 25% this year. However, savvy investors should look at the bigger picture. Every company goes through ups and downs, and Ulta is dealing with strong headwinds right now.

The good news is, it looks like these external factors are starting to lift. Inflation seems to be moderating, interest rates are going down, and the economy might pick up soon. Whenever it does, Ulta could make a quick rebound.

Low price, high potential

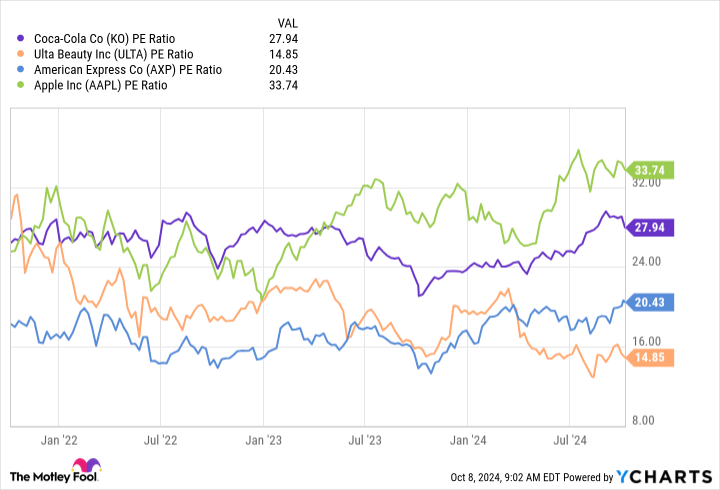

Ulta stock trades at an attractively low P/E ratio of 15. Buffett is known to like a good bargain, or at least what he thinks is an undervalued stock. And Ulta is a lot cheaper than some of his favorite ones.

Buffett knows how to spot a great deal, and Ulta fits the bill. If you buy Ulta stock today, you could benefit from years of long-term gains.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,022!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,329!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $393,839!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 7, 2024

American Express is an advertising partner of The Ascent, a Motley Fool company. Jennifer Saibil has positions in American Express and Apple. The Motley Fool has positions in and recommends Apple, Berkshire Hathaway, Target, and Ulta Beauty. The Motley Fool has a disclosure policy.

This Ridiculously Cheap Warren Buffett Stock Could Make You Richer was originally published by The Motley Fool