Stock market crashes look daunting on a chart so long as we restrict ourselves to a short time horizon. But the more we zoom out, the more they look like minor blips as equities always recover and continue their march upward. That’s why investing in stocks with attractive prospects during bear markets is a good idea. There’s hardly a better time to apply half of the most fundamental piece of investing advice: “Buy low.”

But even if we aren’t in a bear market, buying shares of beaten-down stocks that have what it takes to recover is also an excellent move. Let’s consider two such stocks: DexCom (NASDAQ: DXCM) and Roku (NASDAQ: ROKU).

1. DexCom

DexCom’s shares recently slumped following its second-quarter financial results. What exactly prompted the market to send the company’s shares down? The diabetes-focused medical device specialist revealed that it wasn’t attracting as many new clients as expected.

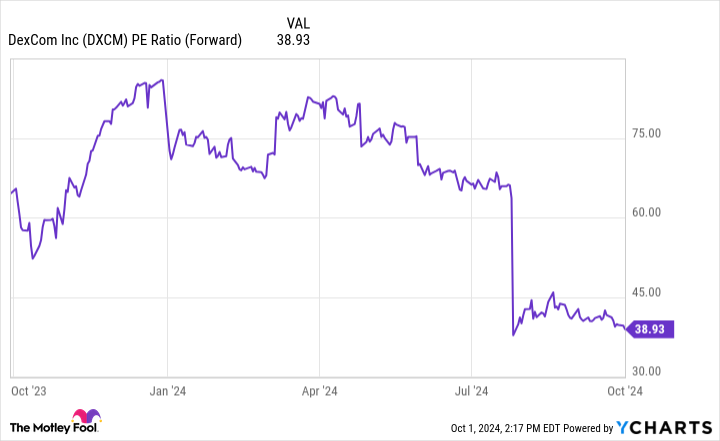

Meanwhile, many consumers took advantage of rebates during the period, which harmed its top line. DexCom’s guidance for the third quarter wasn’t great either. And considering its richly priced stock, it’s not shocking to see a bit of a correction. Yet, DexCom’s forward price-to-earnings (P/E) ratio is still 39, more than twice the healthcare industry’s average P/E of 19.

Those are arguments against the stock, but what about DexCom’s bull case? Where will the company be in 10 years?

First, it’s important to point out that DexCom is one of the leaders in continuous glucose monitoring (CGM), a technology that has proven in many studies to improve health outcomes for diabetes patients. Yet there’s a vast addressable market here. DexCom’s main competitor, Abbott Laboratories, has estimated that only 1% of the “half a billion adults” worldwide with diabetes have access to CGM technology.

DexCom’s addressable market is much smaller, at least for now. However, there is plenty of growth fuel even in countries where it already operates. In the U.S., the percentage of CGM users is well below that of eligible patients who benefit from third-party coverage.

Furthermore, DexCom is building a competitive advantage. The company’s technology is compatible with other devices and digital health apps, from insulin pens and pumps to smartphones and the Apple Watch. The more users in its ecosystem, the more attractive it becomes for third parties to make their devices compatible with DexCom’s technology — an example of the network effect.

Lastly, DexCom is an innovative company that should continue producing new gems. Its G7 has been on the U.S. market since last year and is the most accurate CGM around. It also recently launched an over-the-counter CGM option in the U.S.

Despite its recent drop, DexCom’s long-term prospects are exciting. The stock should provide outsized returns in the next decade, just as it has in the past.

2. Roku

Roku is a leader in streaming — the company’s vast ecosystem features 83.6 million households. Although its financial results haven’t been terrible this year, investors are particularly concerned about a few metrics. Let’s consider two of them.

The first is average revenue per user (ARPU). In the second quarter, Roku’s ARPU remained flat at $40.68 even as its revenue grew 14% year over year to $968.2 million. The second is Roku’s bottom line: The company isn’t profitable. In the second quarter, Roku recorded a net loss per share of $0.24, although that was much better than the loss per share of $0.76 reported in the year-ago period.

Can Roku overcome these two obstacles and deliver solid returns in the next decade? In my view, the answer is yes. Regarding its ARPU, Roku pointed out that it’s starting to gain more users in international markets. For now, it’s concerned with scale in these regions, not monetization. This should be an important growth driver for Roku, though.

Though the streaming industry continues to make headway, it still accounted for just 41% of television viewing time in the U.S. in August. So there’s a vast opportunity there. Once Roku is better established in these regions, the company’s monetization efforts will ramp up, leading to stronger ARPU and revenue growth.

And while the red ink on the bottom line might be an issue, Roku’s platform segment, its most important, is profitable. The platform business brings in revenue from advertisements, operating system licensing deals, and more.

The company records the sale of its namesake streaming player in its device segment — which is not profitable. Roku is choosing to sell these devices at a loss for a good reason. For now, growing its ecosystem is the most important thing. With a vast enough user base, monetization opportunities will increase, as will revenue. That’s Roku’s path to profitability, a milestone it should reach well before 2034.

And in the meantime, the company has the tools to recover and deliver outsized returns. I think you’d do well to invest in the stock while it’s still down.

Should you invest $1,000 in DexCom right now?

Before you buy stock in DexCom, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and DexCom wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $752,838!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 30, 2024

Prosper Junior Bakiny has positions in Roku. The Motley Fool has positions in and recommends Abbott Laboratories, Apple, and Roku. The Motley Fool recommends DexCom. The Motley Fool has a disclosure policy.

2 Beaten-Down Growth Stocks You Might Regret Not Buying was originally published by The Motley Fool