You can never say never when it comes to investing. But when I look at my portfolio, I see Procter & Gamble (NYSE: PG), Hormel Foods (NYSE: HRL), and Hershey (NYSE: HSY) and I think of them as “never-sell” stocks. That’s true even though two of them are currently facing notable adversity (which might make them attractive buys for anyone who doesn’t own them).

Here’s why I’m holding on to this trio of reliable dividend-paying consumer staples stocks, and “never” selling.

Procter & Gamble proves the method

I wouldn’t fault someone for buying Procter & Gamble, usually just called P&G by investors, today. Although the 2.3% dividend yield is only middle of the road historically speaking, it suggests a fair valuation for one of the most iconic consumer staples companies on the planet. But not too long ago P&G was dealing with a bloated and stagnant business, weighed down by brands that weren’t really contributing to the top or bottom lines. At that point, P&G was deeply unloved and the yield was closer to 4%.

That’s when I bought Procter & Gamble, given its status as a Dividend King (with more than 50 years of annual dividend increases). P&G was in a nasty proxy battle with dissident shareholder Nelson Peltz, which it won (but still decided to give Peltz a board seat). The plan at the time was to slim down to focus only on its most important brands, with Peltz pushing for more of a connection between performance and pay. This all seemed reasonable to me, so I jumped in.

The plan worked and P&G turned its fortunes around. I’ve done quite well with that investment, essentially buying a great company when it was out of favor because of solvable short-term problems. Like all of life, companies work through a sine curve shifting between good times and bad times. So if you are patient you can sometimes find winners among unloved stocks.

The key for me is to focus on longtime dividend payers that have historically high, or at least attractive, dividend yields. That is my indication of a high-quality stock that’s trading on the discount rack. This is where Hormel Foods and Hershey come into play.

Hormel and Hershey are out of favor now

Hormel and Hershey are facing some headwinds at the moment. The problems are unique to each (as well as to the problem P&G dealt with), but they don’t appear to be permanent issues. Hormel, for example, hasn’t been able to push through price increases as well as its peers in the face of elevated inflation. It also bought Planters nuts just as the nut segment of the snack business was slowing down, it has been bogged down by avian flu, and it is dealing with a slow pandemic recovery in China. Individually each of these issues would be a nuisance, but collectively they’ve caused investors to panic.

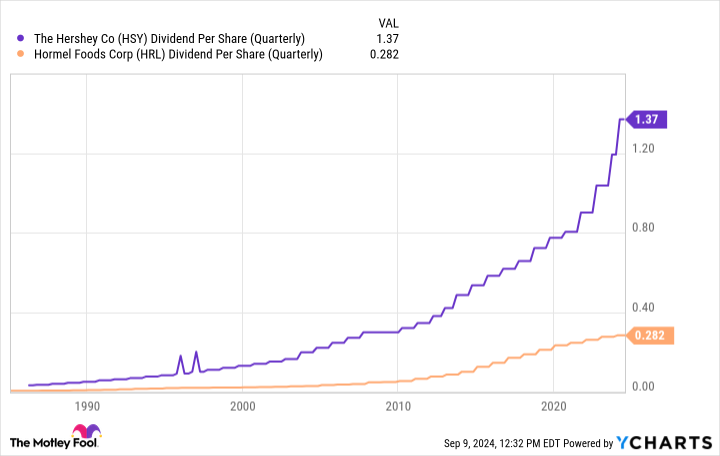

Hershey, meanwhile, has some operational shifts going on thanks to an updated distribution system. That resulted in customers stocking up in advance of the switch-over (just in case the new system failed), which caused a bit of turbulence in revenue. That should pass in time. It has also had to deal with declining demand for popcorn, which it is working through adequately enough by adjusting product sizes and prices.

Most notably, Hershey is being weighed down by the skyrocketing price of cocoa, a key ingredient in making its famous chocolate products. This particular issue has investors really worried because it seems likely that there’s been a step change in cocoa prices given troubled supply dynamics. Investors have been avoiding the shares out of fear that Hershey won’t be able to recoup its rising costs.

These negatives, however, have to be looked at within a broader context. Like P&G, Hormel is a Dividend King. And while Hershey’s dividend streak is only up to 15 years or so, the dividend has trended largely higher throughout its history with some streaks where it has remained the same. Simply put, both are reliable dividend stocks and have been so for a very long time. That’s only possible if a company is well-run and knows how to deal with the inevitable periods of adversity that come from time to time. I’m confident that both food makers will figure out how to survive while continuing to pay their dividends.

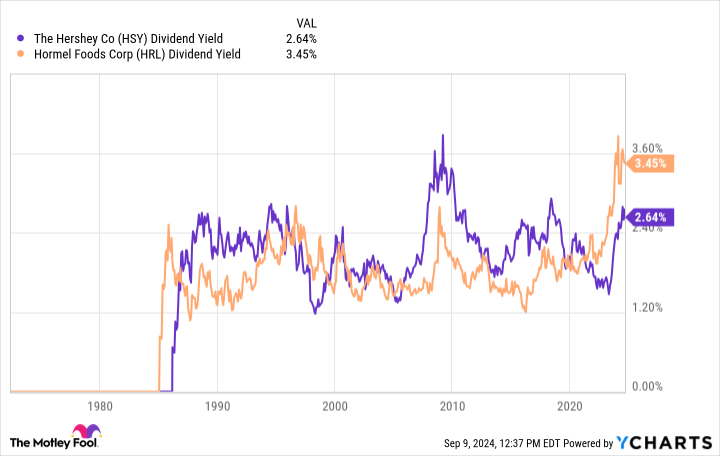

However, despite being great companies, a worried Wall Street has left the stocks with historically attractive dividend yields. Like P&G a few years ago, Hormel and Hershey appear to be on the sale rack. Hormel’s 3.5% yield is near the highest levels in recent history (that’s the deep discount bin). Hershey’s 2.7% yield is toward the high side, but not at an extreme level. It’s just attractively cheap, noting that it very rarely goes on sale at all.

I’ve stepped into both stocks. I’m up on Hershey, a fairly new investment for me, and I’m down slightly on Hormel, a stock I’ve owned for several years. I’m not going to sell either unless something very negative happens operationally at either one. That seems highly unlikely. What I believe is more likely is that these great food makers muddle through their problems while paying me well to wait for better times. Which is exactly what happened with P&G.

Time arbitrage is your secret weapon

If I were running a mutual fund or a hedge fund I would have to justify each and every stock I own to my investors. It would be kind of hard to justify Hershey or Hormel right now, given the generally negative view of them on Wall Street. Even if I loved the stocks, I might end up selling them so I wouldn’t have to deal with the questions. There are drawbacks to being a small, individual investor, but this dynamic isn’t one of them. In fact, the ability to buy and hold for the long term, which I call time arbitrage (I didn’t make up the term, I borrowed it somewhere along the line), is what lets me find gems that Wall Street is overlooking. It’s so simple, but because of the short-term focus on Wall Street, it’s actually a contrarian approach.

The key is to focus on good companies (which I use dividend history to identify) and only buy them when they are out of favor (with historically attractive yields) for what appear to be temporary or at least solvable reasons. And then hold on unless there’s a material negative operational change at the company. This is why I’m holding on to P&G, Hormel, and Hershey. The last two, as noted, still look pretty attractive today, if you’re interested.

Should you invest $1,000 in Procter & Gamble right now?

Before you buy stock in Procter & Gamble, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Procter & Gamble wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $716,375!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 9, 2024

Reuben Gregg Brewer has positions in Hershey, Hormel Foods, and Procter & Gamble. The Motley Fool has positions in and recommends Hershey. The Motley Fool has a disclosure policy.

3 Magnificent Dividend Stocks That I’m “Never” Selling was originally published by The Motley Fool