One of the biggest temptations for dividend investors is reaching for yield. Basically, that means taking on risky investments just to collect a larger income stream. You’ll be better off in the long run if you err on the side of caution, particularly if you need to live off of the income you are generating. That’s why Enterprise Products Partners (NYSE: EPD) is a high-yield investment you’ll wish you’d bought. A quick comparison to Altria (NYSE: MO) will help explain why.

Who wins the high-yield story, Altria or Enterprise?

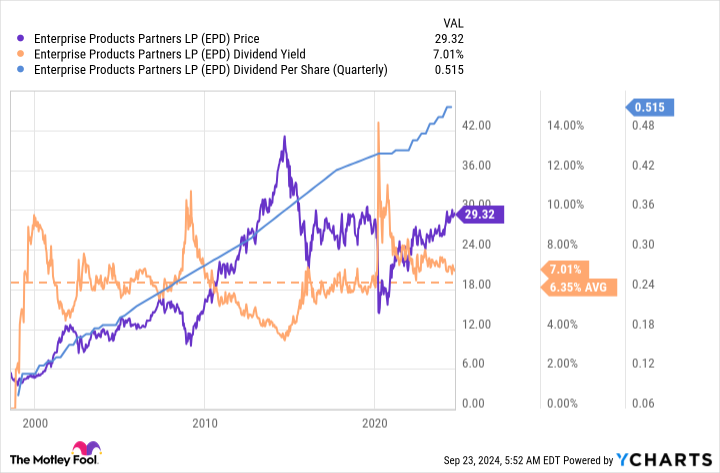

When it comes to yield, Altria’s 8.1% dividend yield is a full percentage point higher than the distribution yield of Enterprise Products Partners’ 7.1%. Both have increased their dividends regularly, so many investors might default to the higher-yielding option. But that’s not necessarily the best plan.

Altria, a consumer staples company, comes with more risk than you may think despite operating in what is generally considered a reliable sector. That’s because its main product is cigarettes. This business has been in a secular decline for a long time. In the second quarter of 2024 alone, Altria’s cigarette volumes fell 13% year over year. That’s not a fluke. In the second quarter of 2023, volumes fell 8.7%. In the same quarter of 2022, cigarette volume was off by 11.1%. Any recent quarter and any recent full year would have shown the same terrible trend.

The company has offset volume declines with price increases, which has allowed it to continue growing its dividend despite the clearly terrible direction of its most important business line. There’s a very real chance that you will regret buying this high-yield dividend stock if it can’t stem the bleeding in some way.

Enterprise is a totally different story.

Enterprise’s lower yield comes with lower risk

You can easily argue that Enterprise comes with its own risks, given that it operates in the highly volatile energy sector. And its midstream business is directly tied to demand for oil and natural gas, which is being pressured by the move toward cleaner alternatives. Fair enough, but what does Enterprise actually do?

As a midstream provider, Enterprise owns vital infrastructure assets that help move oil and natural gas around the world. It generally charges fees for the use of its infrastructure, so the price of energy is less important than the demand for energy. Demand for energy tends to remain robust regardless of the price of oil and natural gas.

But here’s the big fact — despite all the hype around clean energy, demand for oil and natural gas is expected to remain robust for decades to come. In fact, demand will likely increase for these fuels, with far dirtier coal bearing the brunt of the clean energy switch.

In other words, Enterprise’s business isn’t as risky as it may seem. On top of that, it is one of the largest midstream players in North America with an investment-grade-rated balance sheet. While internal growth options are limited, it has long acted as an industry consolidator. It just announced plans to buy Pinon Midstream for $950 million, for example. Acquisitions are lumpy and impossible to predict, but they give Enterprise ample room for growth on top of the slow and steady price increases it will be able to extract from customers.

If you want a high yield from a growing business, Enterprise is the better option when compared to Altria and its declining core business. Sure, you’ll give up a percentage point of yield, but as Altria continues to struggle, that last point will allow you to sleep at night if you buy Enterprise.

Enterprise’s yield still looks cheap

Here’s the most interesting part: Enterprise’s 7.1% dividend yield is above its 10-year average yield of 6.3%. So despite the recovery from pandemic lows, it still appears to be undervalued. A growing business, a financially strong company, and an undervalued price all make Enterprise a high-yield stock you’ll regret missing out on. Especially when you compare it to other high-yield choices with similarly high, but far riskier, yields.

Should you invest $1,000 in Altria Group right now?

Before you buy stock in Altria Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Altria Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $743,952!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 23, 2024

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

A Few Years From Now, You’ll Wish You’d Bought This Undervalued High-Yield Stock was originally published by The Motley Fool