One of the most important dates in modern history is Nov. 30, 2022 — the day that OpenAI released ChatGPT to the public. It didn’t take long for people all over the world to become totally enamored by the potential of generative artificial intelligence (AI).

Perhaps no company has benefited as much from the AI revolution as semiconductor and data center specialist Nvidia (NASDAQ: NVDA). Since the commercial launch of ChatGPT about two years ago, shares of Nvidia are up by more than 700%.

Nvidia has completely dominated the high-performance computing market, largely through its industry-leading graphics processing units (GPU). However, three trends visible in the company’s latest earnings report have me concerned that the euphoric bubble surrounding Nvidia might be about to burst.

1. Revenue and profit growth are slowing down

Nvidia reports its revenue in five different categories, but the vast majority of its sales now come from its data center business. Within the data center category, Nvidia bifurcates its revenue into two further sub-categories: compute and networking.

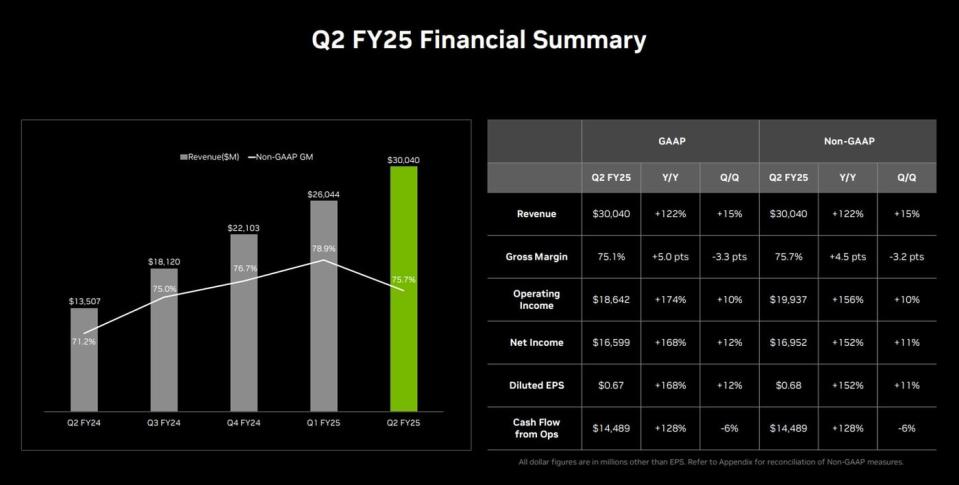

For the last two years, sales from compute and networking have been off the charts, consistently clocking triple-digit percentage growth as demand for Nvidia’s GPUs remained robust. A couple of weeks ago, Nvidia reported results for its fiscal 2025 second quarter, which ended July 28. The company’s total quarterly revenue of $30 billion set a new record, as did its data center total of $26.3 billion.

While these figures might make Nvidia look unstoppable, the underlying trends suggest otherwise. The table below breaks down Nvidia’s annual and sequential growth rates for total revenue and data center revenue over the last five quarters.

|

Metric |

Q2 2024 |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|---|---|---|---|---|---|

|

Total revenue growth (YoY) |

101% |

206% |

265% |

262% |

122% |

|

Total revenue growth (QoQ) |

88% |

34% |

22% |

18% |

15% |

|

Data center revenue growth (YoY) |

171% |

279% |

409% |

427% |

154% |

|

Data center revenue growth (QoQ) |

141% |

41% |

27% |

23% |

16% |

Data source: Nvidia. YOY = year over year. QoQ = quarter over quarter.

It’s hard to criticize a company that is growing as fast as Nvidia is. What I’m concerned about isn’t its ability to create demand, but the pace at which this demand occurs. Sales in the data center business — and by extension, Nvidia’s entire sales base — are starting to show signs of deceleration. Some of this can be chalked up to the cyclicality of the semiconductor industry broadly, while some of the sales trends can be attributed to ongoing bottlenecks in Nvidia’s supply chain.

Nevertheless, I am a bit wary of a slowing sales pace. Moreover, further analysis suggests that where Nvidia’s growth comes from could be an even larger issue.

2. Customer concentration is becoming more apparent

Looking at top-line figures alone doesn’t help much in determining the health of a business. A more useful stat to analyze is customer concentration. This reflects how diversified a company’s sales base is.

Although Nvidia sells its GPUs around the globe, analysis of the company’s financial reports suggests that the business has become heavily concentrated. In fiscal 2025’s second quarter, almost half of Nvidia’s $30 billion in revenues came from just four customers. This level of concentration isn’t really anything new, and I see rising competition as a big reason Nvidia’s sales deceleration could be further exacerbated.

While Nvidia faces direct competition from Advanced Micro Devices, the company is also beginning to witness a surge in competition from tangential sources such as Microsoft, Tesla, Meta Platforms, and Amazon.

Many of these “Magnificent Seven” companies are large buyers of Nvidia’s tech. However, based on remarks from executives at these various megacaps, many of these companies are looking to reduce their dependence on Nvidia and actually design their own chips that compete directly with its tech.

Even when that competition begins to take shape, I think Nvidia will have little problem finding new buyers. But with rising competition comes another issue: a loss of pricing power. As more AI-capable GPUs become widely available — possibly to the point of becoming commoditized hardware — it’s likely that Nvidia will not be able to command such high prices for its chips.

These dynamics lead me to my final, and most significant, concern about Nvidia’s outlook.

3. The most important metric: gross margin

With its existing pricing power, Nvidia has steadily commanded strong margins. However, the company’s latest earnings report revealed a notable drop in gross margin.

I wouldn’t fret too much about a single quarter’s decelerating margin profile, but the larger implications here are tough to ignore.

If margins continue to deteriorate amid a backdrop of rising competition, Nvidia’s bottom line could be significantly impacted. Its free cash flow and profitability would begin to shrink, leaving it with less capacity to invest in research and development, marketing, and other innovation areas or growth tactics.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $730,103!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 9, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Is Nvidia’s Bubble About to Burst? 3 Numbers That Have Me Thinking It Just Might Be. was originally published by The Motley Fool