While it’s perfectly normal for a hot trend to be captivating the attention of Wall Street and investors, two buzzy trends at the same time are somewhat rare. In addition to investors piling into stocks associated with the artificial intelligence (AI) revolution, they seemingly can’t get enough of companies announcing stock splits.

A stock split is a tool on the proverbial utility belt for publicly traded companies that allows them to adjust their share price and outstanding share count by the same magnitude. Despite these nominal changes, stock splits are purely cosmetic and have no impact on a company’s market cap or its operating performance.

Although stock splits can occur in both directions — reverse-stock splits increase a company’s share price, while forward-stock splits reduce it — a majority of investors favor companies completing forward splits. Businesses undertaking forward splits are usually outperforming their peers in every respect, which is what propels their underlying stock higher.

In 2024, 13 leading companies have announced or completed a stock split, all but one of which is a forward-stock split. Today just happens to be the day one of these phenomenal businesses will be trading at its post-split price for the first time.

This nearly 125,000%-gainer just completed its sixth split since going public

Earlier this week, satellite-radio operator Sirius XM Holdings enjoyed its time in the sun as the only prominent reverse-stock split of 2024. But today, Sept. 12, it’s all about recognizing corporate identity uniform and business services provider Cintas (NASDAQ: CTAS).

Back on May 2, the company’s board announced plans to complete a 4-for-1 split following the close of trading on Sept. 11. With the company’s shares closing at north of $816 on Sept. 10, the largest split in the company’s history will reduce its share price to a shade over $200.

Since its initial public offering (IPO) in 1983, Cintas has delivered a total return (i.e., factoring in dividend payments along with the cumulative return of its shares) of almost 125,000% and completed a half-dozen stock splits:

The catalyst fueling this growth is, first and foremost, the growth of the U.S. economy. Although recessions are a perfectly normal and inevitable aspect of the economic cycle, history tells us that these downturns tend to be short-lived. Only three of 12 U.S. recessions since the end of World War II have lasted at least 12 months.

On the other hand, most periods of growth endure for multiple years. An expanding economy tends to lead to higher demand for corporate uniforms and the various products and services Cintas provides, such as towels, floor mats, and safety kits.

Beyond macroeconomic catalysts, Cintas has also benefited from a steady diet of bolt-on acquisitions. Purchasing Zee Medical and G&K Services are perfect examples of Cintas expanding its product and service ecosystem, dangling a carrot for new clients, and providing itself the opportunity to cross-sell more of its products to existing clients.

Innovation is another key puzzle piece for Cintas. Ongoing product development for its line of rental uniforms, as well as its various business product lines, tends to keep customers loyal.

Last but not least, Cintas has more than 1 million corporate clients. This level of diversification all but ensures that no one single business is paramount to its success or capable of sinking the proverbial ship.

Despite Cintas’s long-term success, additional near-term upside could be a tough ask

While Cintas has a pretty clear path to long-term growth, thanks largely to being tied at the hip to the U.S. economy, additional upside for shares of the company over the next couple of years could be a tough ask.

For one, there are mounting concerns that a U.S. recession is brewing. A couple of data points and predictive metrics, including the first notable decline in U.S. M2 money supply since the Great Depression, as well as the longest yield-curve inversion in history, suggest coming weakness for the economy and stock market.

Though stocks don’t move in-tandem with the U.S. economy, Cintas is undeniably cyclical. Most of its clients are liable to feel some degree of pain if economic growth slows or contracts, which would, in turn, be expected to slow down its own growth rate.

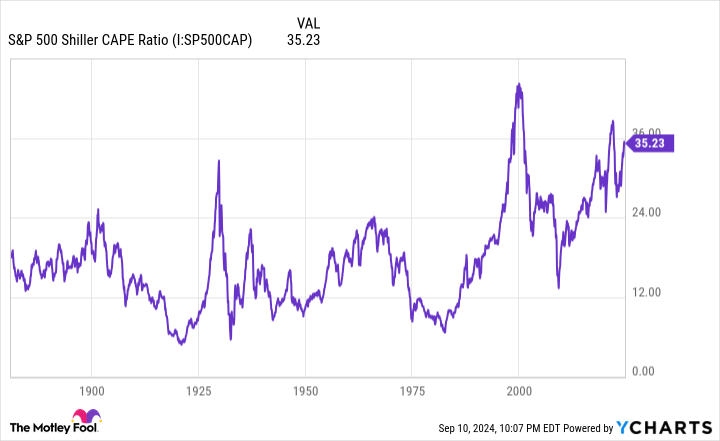

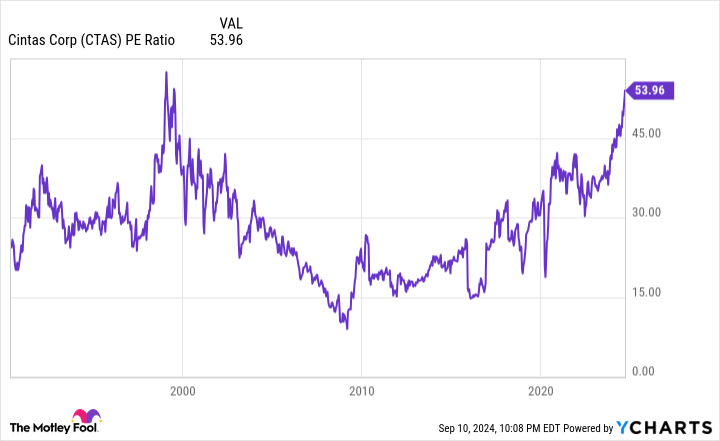

To build on this point, both the broader market and Cintas are historically expensive.

According to the S&P 500‘s Shiller price-to-earnings (P/E) ratio, which is also commonly referred to as the cyclically adjusted price-to-earnings ratio (CAPE ratio), the stock market has only been as pricey as it is now two other times, when back-tested to January 1871.

On Sept. 10, the S&P 500’s Shiller P/E, which is based on average inflation-adjusted earnings from the prior 10 years, closed at 35.33, or more than double than 153-year average of 17.16. More importantly, previous instances where the S&P 500’s Shiller P/E topped 30 during a bull market rally were, eventually (key word!), followed by declines of at least 20%.

Cintas ended Sept. 10 at roughly 54 times its trailing-12-month (TTM) earnings per share (EPS) and a nosebleed 44 times forward-year EPS. You’d have to go back to the late 20th century to find the last time Cintas was valued at 54 times TTM EPS.

While a forecast sales growth rate of 7% in the current and upcoming year is admirable for a company of its size, it doesn’t come to close to justifying a forward P/E ratio of 44.

This is a rare instance of a rock-solid business whose stock simply isn’t worth buying at the moment.

Should you invest $1,000 in Cintas right now?

Before you buy stock in Cintas, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Cintas wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $662,392!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 9, 2024

Sean Williams has positions in Sirius XM. The Motley Fool recommends Cintas. The Motley Fool has a disclosure policy.

One of Wall Street’s Highest-Flying Stocks — a Nearly 125,000%-Gainer Since Its IPO — Has Officially Completed Its Latest Stock Split was originally published by The Motley Fool